/ COMMODITIES

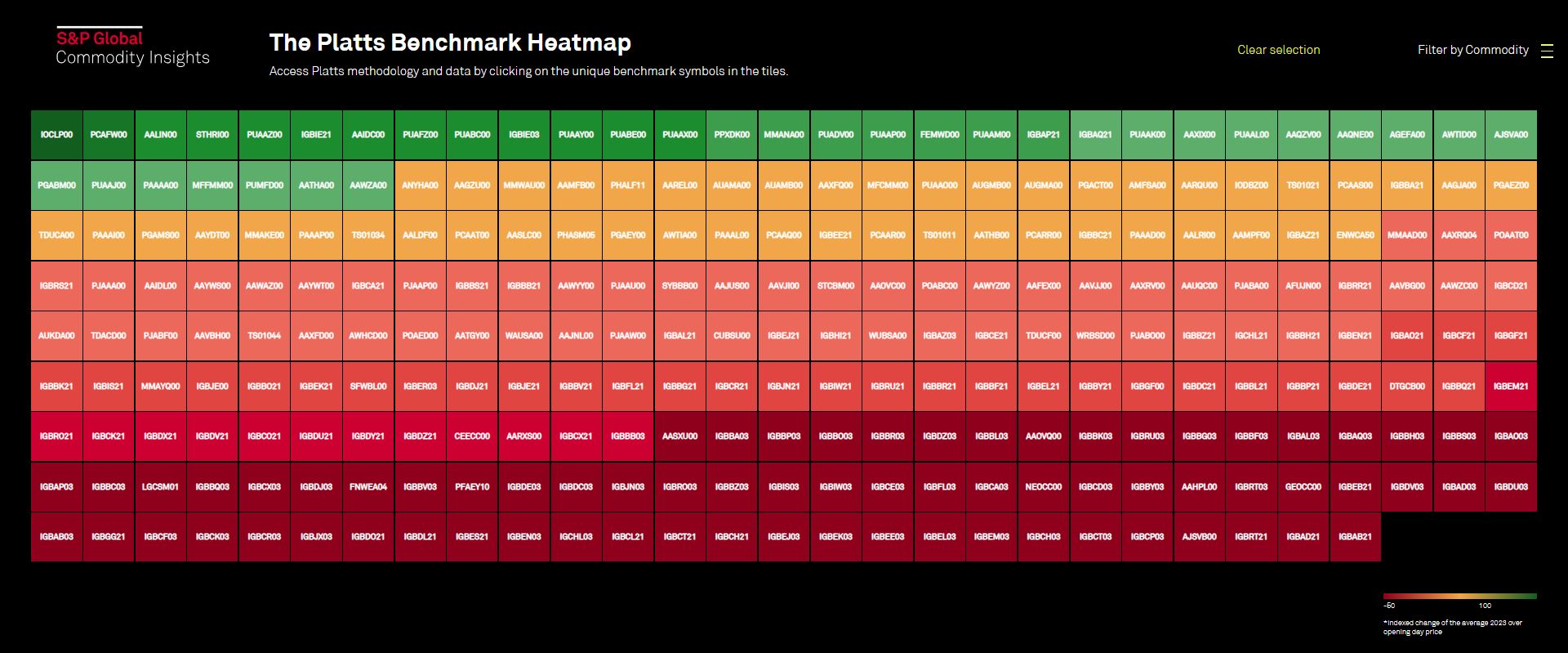

Interactive: The Platts Benchmark Heatmap

The price wall visualizes 258 of the most important price benchmarks assessed by Platts across various commodities...

/ COMMODITIES

/ COMMODITIES

The price wall visualizes 258 of the most important price benchmarks assessed by Platts across various commodities...

/ COMMODITIES

In May 2023, the world's most important oil price benchmark, Platts Dated Brent, which is used to underpin the price of significant volumes of traded crude oil, saw the addition of the first non-North Sea crude stream into its deliverable basket of grades: WTI Midland. Since then, the benchmark has seen liquidity skyrocket, the addition of new faces into the Brent complex’s long list of established market participants and, most importantly, the further strengthening of Dated Brent as a price indicator for commodity markets globally. In this episode of the Oil Markets Podcast, Joel Hanley is joined by Emma Kettley, Managing Crude Editor, and Sam Angell, Senior Crude Editor to discuss the one-year anniversary of Midland’s successful inclusion into the Dated Brent benchmark.Related content: Infographic: Dated Brent April update Related story: April 2024 breaks trade liquidity records in Platts North Sea physical, Cash BFOE partials MOCMentioned price assessments: PCAAS00 - Dated Brent WMCRB00 - WTI Midland CIF Rotterdam vs Fwd Dated Brent $/bbl More listening options:

The spotlight on India's oil sector has never been stronger. India's role in global oil markets is set to expand at a fast pace until the end of the decade, making it the biggest center for demand growth, according to the IEA. Refining expansion remains a key priority, but with a tilt towards petrochemicals, and the country’s upstream strategy aims to realize the hydrocarbon potential of offshore regions. While rising Russian oil flows and its impact on purchases from the Middle East is dominating the discussion on trade flows, rising oil prices is throwing up new challenges for the economy. In a wide-ranging discussion with Sambit Mohanty, Asia Energy Editor, Atul Arya, Chief Energy Strategist at SP Global Commodity Insights, and Dharmakirti Joshi, Chief India Economist at CRISIL -- a unit of SP Global – share their views on the roadmap ahead for India's oil sector as the country is set to elect a new federal government.More listening options: