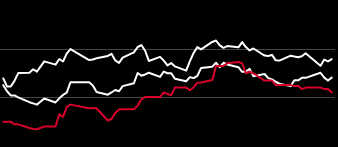

Platts Global Recycled Packaging Index

/ COMMODITIES

Explore the Chemical Universe

All the elements. All in one place.

/ COMMODITIES

/ COMMODITIES

All the elements. All in one place.

/ COMMODITIES

The safety of food chemicals has become an increasingly hot topic in the US, as several states are considering individual bans on common food additives in conflict with federal regulations. California opened the door for these bans last year, as it adopted the California Food Safety Act -- a law that requires food companies to eliminate by 2027 Red dye No. 3, brominated vegetable oil (BVO), potassium bromate and propyl paraben from their products.With other states now considering similar bans, SP Global Commodity Insights offer a quick overview of this burning issue, highlighting what it means for companies and what are the latest developments that food makers and retailers should watch out for.

An SP Global Commodity Insights joint webinar with Plastics Recyclers Europe, Recycled polymers market dynamics - Legislative outlook, pricing evolution and relationship with virgin materialWatch this webinar on-demand and keep abreast of the latest news and pricing trends in the recycled polymers market is essential for investment decisions, competitiveness, and profitability. Upcoming regulations and legislation will significantly influence pricing and market behaviour. Anticipating the impact of regulatory changes is crucial for adapting business strategies and ensuring compliance. Moreover, tracking the decoupling between recycled and virgin polymer prices sheds light on market maturity and demand trends.Download the presentation here

Katja Wodjereck, executive vice president/renewable products at Neste, is interviewed by SP Global Commodity Insights editors Iris Poon and Dias Kazym on Neste's views on renewable fuels and chemicals. Topics include the company's strategy in renewables, the role of regulation, and whether renewable feedstocks are competitive in the market.The Chemical Week podcast is the industry’s premier platform for wide-ranging discussion of issues impacting the global chemicals sector, hosted by the editors of Chemical Week and SP Global Commodity Insights. Subscribe to the Chemical Week podcast on your favorite platform, or visit chemweek.com/podcast to view our episode archive.