Japan to introduce new refining regulations, incorporate decarbonization efforts

Japan will start formal policy discussions July 28 to introduce a fourth round of refining regulations aimed at boosting the processing volume of vacuum residue, with preferential treatment expected for efforts to decarbonize the refining process, sources told S&P Global Commodity Insights July 26.

The talks will be launched by the Ministry of Economy, Trade and Industry's natural resources and fuel committee, which will present ideas for new regulations and review regulatory responses from the last round that expired at the end of March, the METI sources said.

The new regulations would likely follow the framework of the third round of regulations, with new elements relating to decarbonization efforts by refiners to be considered as part of the regulatory response, the sources said.

The refiners' potential use of blue and green hydrogen instead of gray hydrogen in the refining process could be considered among the decarbonization efforts, the sources added.

The third round of regulations required refiners to achieve a national target vacuum residue ratio, the daily residual processing volume as a percentage of the daily crude processing volume, of 7.5% by the end of March 2022.

Given a significant drop in Japanese refiners' refining volumes in the past two years because of the pandemic-led demand slump, Petroleum Association of Japan President Tsutomu Sugimori said March 22 that "It will be difficult to achieve."

"However, we are in the midst of emergency situations such as the coronavirus pandemic and the Ukraine issues, so that we expect to see some sort of mitigation," Sugimori added at the time.

The third round of regulations introduced in 2017 focused on increasing processed volumes at residue cracking units across Japan's refining fleet with improvements in productivity. The previous two rounds of regulations had led to a reduction in Japan's overall crude distillation capacity.

The third round of regulations required refiners to increase processing volumes of vacuum residue by the end of fiscal year 2021-22 (April-March) from baseline average volumes processed over FY 2014-15 to FY 2016-17.

Under its definition, vacuum residue has a true boiling point of more than 565 degrees Celsius. This includes atmospheric residue, vacuum residue, vacuum gasoil and other residues processed at fluid catalytic cracking and residue fluid catalytic cracking and cokers.

In order to comply with the third round of regulations, refiners had been expected to revamp their facilities, including carrying out work to upgrade pumps and change catalysts to be able to process more residues at units such as FCCs, RFCCs and cokers by the end of March 2022.

Japan's nameplate refining capacity was 3.5188 million b/d across 22 refineries as of March 31, 2017 down 7.1% from 3.7897 million b/d earlier, following local refiners' response to the earlier rounds of refining regulations.

The country's operable refining capacity stood at 3.4578 million b/d across 21 refineries at the end of March 2022.

News

India's unwavering appetite for Russian crude has provided ample bandwidth to Middle Eastern sour crude suppliers to cater to the needs of South Korea, Japan, Thailand and other East Asian buyers. Even if OPEC+ decides to extend production cuts, East Asian refiners are confident they can secure adequate Middle East sour crude term supplies. View full-size infographic Also listen:

News

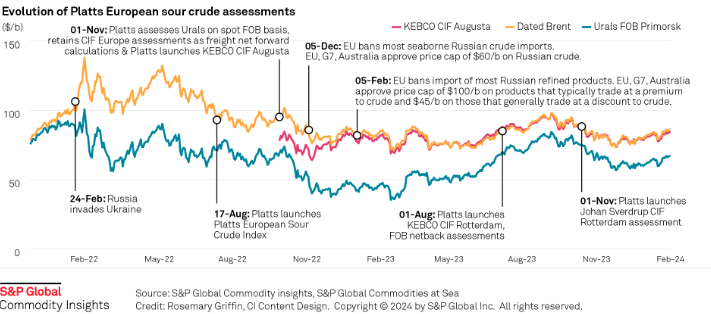

Russia's invasion of Ukraine has had a profound impact on sour crude export destinations, and increased the appetite for sweet crudes among European refiners. Platts methodology has evolved to reflect this changing landscape. Click here to see the full-size infographic.

News

Latest update: Jan. 30, 2024 A key OPEC+ advisory committee, co-chaired by Saudi Arabia and Russia, is set to meet online Feb. 1, with crude prices still stuck below the level that many of the alliance’s major producers need to balance their budgets. Traders will be seeking signals from the Joint Ministerial Monitoring Committee meeting on how long the bloc will keep the reins on its production and how it sees supply-demand fundamentals shaping up in the months ahead. Related story: OPEC+ monitoring committee prepares to meet as group battles sticky oil prices (Subscriber content) Click here to view the full-size infographic Compare hundreds of different crude grades and varieties produced around the world with Platts interactive Periodic Table of Oil .

News

Sumas spot gas down 90.6% year on year CAISO solar generation up 6 points in Dec US West power forwards are trending roughly 50% lower than year-ago packages on weaker gas forwards and above-normal temperatures forecast with El Nino weather conditions to linger into spring. El Nino conditions, which typically occur January through March, tend to bring more rain to the US Southwest and warmer-than-normal temperatures. The three-month outlook indicates a greater probability for above-normal temperatures across most of the Western US, with the exception of the Desert Southwest, according to the US National Weather Service's Climate Prediction Center. SP15 on-peak January rolled off the curve at $55.75/MWh, 79.4% lower than where the 2023 package ended, according to data from Platts, part of S&P Global Commodity Insights. The February package is currently in the low 50s/MWh, 70% below where its 2023 counterpart was a year earlier, while the March package is in the mid-$30s/MWh, 55.4% lower. In gas forwards, SoCal January rolled off the curve at $3.779/MMBtu, 97.9% below where the 2023 contract ended a year earlier, according to S&P Global data. The February contract is currently around $4.063/MMBtu, 78.9% lower than its 2023 counterpart at the same time last year, while the March contract is about $2.816/MMBtu, 63.2% lower. Gas plants burned an average of 1.815 Bcf/d in December to generate an average of 267.167 GWh/d, an analysis of S&P Global data showed. That's down 0.66% from November and a drop of 11.2 % from 2023. S&P Global forecast CAISO's gas fleet to generate around 220 GWh/d in February. In comparison, burning fuel at the same rate as February 2023 would consume 1.758 Bcf/d, a 6% decrease year on year. Spot markets In spot markets, power prices were down significantly from a year ago, when cold weather hit the region and drove up prices. SP15 on-peak day-ahead locational marginal prices averaged $43.49/MWh in December, 83% lower year over year and 11.2% below November prices, according to California Independent System Operator data. Helping pull down power prices, spot gas at SoCal city-gate was down 88.4% year on year and 40% lower month on month at an average of $3.554/MMBtu in December, according to S&P Global data. In the Northwest, Sumas spot gas was down 90.6% year on year at an average of $2.669/MMBtu. The decline in spot gas prices likely accounts for the lower average spot power prices month on month in December, said Morris Greenberg, senior manager with the low-carbon electricity team at S&P Global. Compared to a year earlier, CAISO population-weighted temperatures averaged 8% higher in December, resulting in 38.4% fewer heating-degree days, according to CustomWeather data. Fuel mix Thermal generation remained the lead fuel source at 46.1% of the total fuel mix in December, little changed year on year, while solar generation was up nearly 6 percentage points to average 14.7% of the mix, according to CAISO data. Hydropower remained strong, averaging 8% of the December fuel mix, 2 points higher than a year earlier. Total generation was down nearly 8% from a year earlier at an average of roughly 23.4 GWh/day, as peakload slipped 2% year on year to average 27.254 GW in December, according to CAISO data. In the Northwest, peakload dropped nearly 11% year on year to average 7.89 GW in December, according to Bonneville Power Administration data. Hydropower remained the lead fuel source at nearly 74% of the mix, followed by nuclear at 12.3%, thermal at 9.6% and wind at 4.3%. Following El Nino expectations of the Northwest for warmer temperatures and drier precipitation, BPA population-weighted temperatures in December were 10% above normal and 21.5% higher than a year earlier, leading to 27% fewer heating-degrees days year on year, according to CustomWeather data.