Asian gasoline cracks to come under pressure as China set to lift end-2022 outflows

China is expected to export between 1.7 million mt (466,000 b/d) and 2 million mt (548,000 b/d) of gasoline in November and over 2 million mt in December, substantially higher compared with the 1 million mt it exported in October, analysts and market sources said Dec. 1. And should this happen, would likely exert downward pressure on regional gasoline crack spreads.

Asia's largest gasoline exporter is expected to further lift its gasoline outflows by the end of 2022 in a bid to support its economy by encouraging exporters to exhaust their remaining export quotas.

According to General Administration of Customs data, the country's gasoline exports stood at 662,000 mt in September, jumping 51.8% to 1 million mt in October.

"Chinese oil companies will try their best to maximize the usage of their oil product export quotas, in a bid to push up the country's total goods export volumes and economy performance," said Sun Sijia, an analyst with S&P Global Commodity Insights.

Beijing released 37.25 million mt of clean oil product export quotas in 2022. In January-October, China exported 23.2 million mt of gasoline, gasoil and jet fuel, the GAC data showed, leaving 14.05 million mt of quota yet to be used in November and December.

"To boost exports as an economic indicator and earn more US dollars, related government authorities may work together with the refineries to facilitate and smoothen the logistics, helping the volume to hit a record high," a Beijing-based analyst said.

China's domestic demand in November was weak amid tight movement restrictions, with capital city Beijing and manufacturing hubs Guangzhou, Chongqing under strict COVID control, while refining throughput was likely to hit a nine-month high. This would leave sufficient gasoline for export, market sources said.

Sun said the Chinese government may alter COVID-19 restrictions frequently, resulting in an erratic impact on domestic gasoline demand. She added that people in China would continue to prefer to stay home to avoid infection and private cars remain the choice mode of transportation given rigid travel guidelines.

Meanwhile, the country's estimated gasoline export volumes in 2023 remain subjected to next year's export quotas, which Chinese exporters are eagerly awaiting updates on, sources said.

Expectations of China continuing to export large volumes of gasoline moving forward could possibly bolster overall gasoline supplies and exert a downward pressure on cracks, industry sources said.

Several market participants also said that gasoline prices could also be weighed down by reduced demand from Malaysia following the end of the Nov. 19 general elections.

However, other market participants said Malaysia's gasoline demand could be bolstered amid the school holiday period.

Reflecting the softening sentiment, Platts-assessed front month FOB Singapore 92 RON gasoline swap crack spread against Brent swaps stood at 78 cents/b Dec. 1, down from $1.47/b on Nov. 30, S&P Global data showed.

The physical FOB Singapore 92 RON gasoline crack against front month ICE Brent crude oil futures was assessed at $2.07/b Dec. 1, down from $3.33/b at the Asian close Nov. 30.

News

India's unwavering appetite for Russian crude has provided ample bandwidth to Middle Eastern sour crude suppliers to cater to the needs of South Korea, Japan, Thailand and other East Asian buyers. Even if OPEC+ decides to extend production cuts, East Asian refiners are confident they can secure adequate Middle East sour crude term supplies. View full-size infographic Also listen:

News

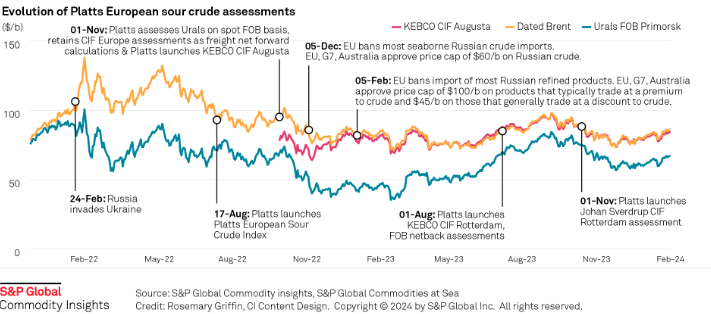

Russia's invasion of Ukraine has had a profound impact on sour crude export destinations, and increased the appetite for sweet crudes among European refiners. Platts methodology has evolved to reflect this changing landscape. Click here to see the full-size infographic.

News

Latest update: Jan. 30, 2024 A key OPEC+ advisory committee, co-chaired by Saudi Arabia and Russia, is set to meet online Feb. 1, with crude prices still stuck below the level that many of the alliance’s major producers need to balance their budgets. Traders will be seeking signals from the Joint Ministerial Monitoring Committee meeting on how long the bloc will keep the reins on its production and how it sees supply-demand fundamentals shaping up in the months ahead. Related story: OPEC+ monitoring committee prepares to meet as group battles sticky oil prices (Subscriber content) Click here to view the full-size infographic Compare hundreds of different crude grades and varieties produced around the world with Platts interactive Periodic Table of Oil .

News

Sumas spot gas down 90.6% year on year CAISO solar generation up 6 points in Dec US West power forwards are trending roughly 50% lower than year-ago packages on weaker gas forwards and above-normal temperatures forecast with El Nino weather conditions to linger into spring. El Nino conditions, which typically occur January through March, tend to bring more rain to the US Southwest and warmer-than-normal temperatures. The three-month outlook indicates a greater probability for above-normal temperatures across most of the Western US, with the exception of the Desert Southwest, according to the US National Weather Service's Climate Prediction Center. SP15 on-peak January rolled off the curve at $55.75/MWh, 79.4% lower than where the 2023 package ended, according to data from Platts, part of S&P Global Commodity Insights. The February package is currently in the low 50s/MWh, 70% below where its 2023 counterpart was a year earlier, while the March package is in the mid-$30s/MWh, 55.4% lower. In gas forwards, SoCal January rolled off the curve at $3.779/MMBtu, 97.9% below where the 2023 contract ended a year earlier, according to S&P Global data. The February contract is currently around $4.063/MMBtu, 78.9% lower than its 2023 counterpart at the same time last year, while the March contract is about $2.816/MMBtu, 63.2% lower. Gas plants burned an average of 1.815 Bcf/d in December to generate an average of 267.167 GWh/d, an analysis of S&P Global data showed. That's down 0.66% from November and a drop of 11.2 % from 2023. S&P Global forecast CAISO's gas fleet to generate around 220 GWh/d in February. In comparison, burning fuel at the same rate as February 2023 would consume 1.758 Bcf/d, a 6% decrease year on year. Spot markets In spot markets, power prices were down significantly from a year ago, when cold weather hit the region and drove up prices. SP15 on-peak day-ahead locational marginal prices averaged $43.49/MWh in December, 83% lower year over year and 11.2% below November prices, according to California Independent System Operator data. Helping pull down power prices, spot gas at SoCal city-gate was down 88.4% year on year and 40% lower month on month at an average of $3.554/MMBtu in December, according to S&P Global data. In the Northwest, Sumas spot gas was down 90.6% year on year at an average of $2.669/MMBtu. The decline in spot gas prices likely accounts for the lower average spot power prices month on month in December, said Morris Greenberg, senior manager with the low-carbon electricity team at S&P Global. Compared to a year earlier, CAISO population-weighted temperatures averaged 8% higher in December, resulting in 38.4% fewer heating-degree days, according to CustomWeather data. Fuel mix Thermal generation remained the lead fuel source at 46.1% of the total fuel mix in December, little changed year on year, while solar generation was up nearly 6 percentage points to average 14.7% of the mix, according to CAISO data. Hydropower remained strong, averaging 8% of the December fuel mix, 2 points higher than a year earlier. Total generation was down nearly 8% from a year earlier at an average of roughly 23.4 GWh/day, as peakload slipped 2% year on year to average 27.254 GW in December, according to CAISO data. In the Northwest, peakload dropped nearly 11% year on year to average 7.89 GW in December, according to Bonneville Power Administration data. Hydropower remained the lead fuel source at nearly 74% of the mix, followed by nuclear at 12.3%, thermal at 9.6% and wind at 4.3%. Following El Nino expectations of the Northwest for warmer temperatures and drier precipitation, BPA population-weighted temperatures in December were 10% above normal and 21.5% higher than a year earlier, leading to 27% fewer heating-degrees days year on year, according to CustomWeather data.