/ COMMODITIES

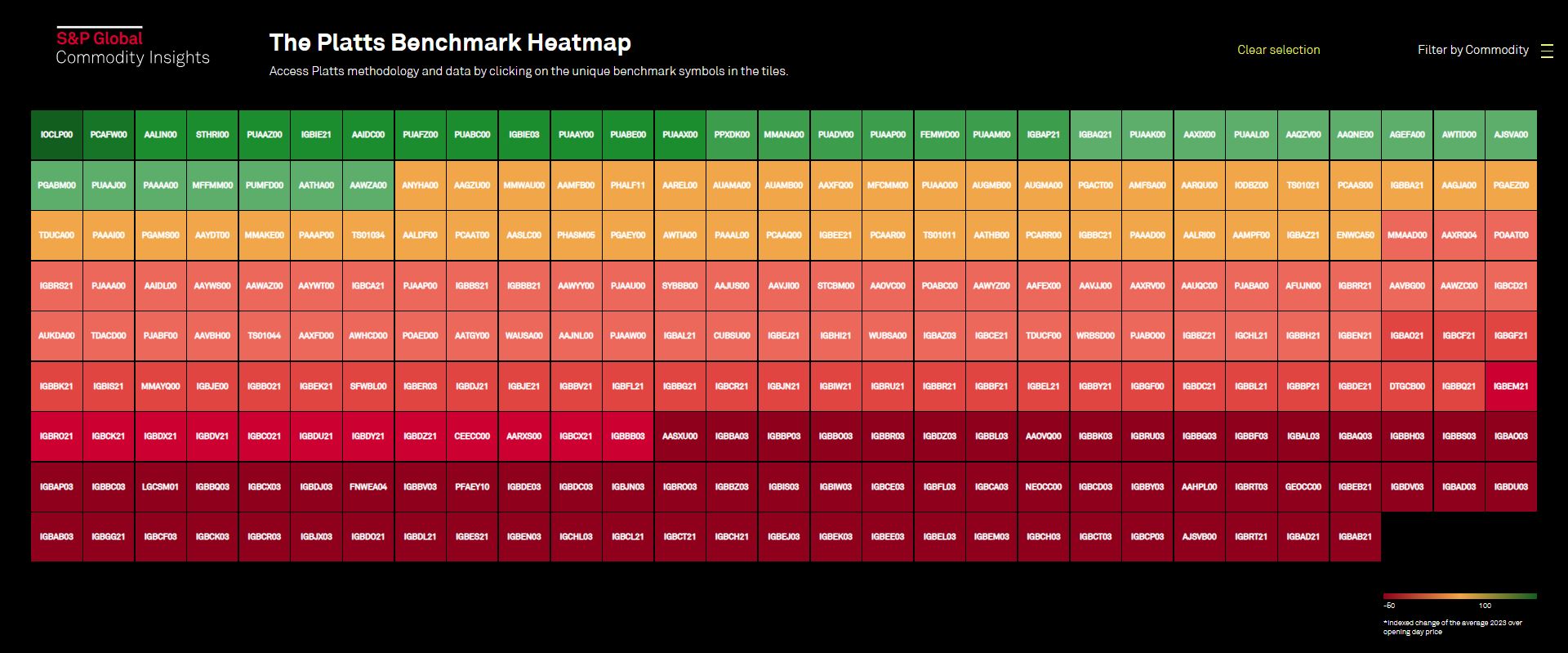

Interactive: The Platts Benchmark Heatmap

The price wall visualizes 258 of the most important price benchmarks assessed by Platts across various commodities...

/ COMMODITIES

/ COMMODITIES

The price wall visualizes 258 of the most important price benchmarks assessed by Platts across various commodities...

/ COMMODITIES

The spotlight on India's oil sector has never been stronger. India's role in global oil markets is set to expand at a fast pace until the end of the decade, making it the biggest center for demand growth, according to the IEA. Refining expansion remains a key priority, but with a tilt towards petrochemicals, and the country’s upstream strategy aims to realize the hydrocarbon potential of offshore regions. While rising Russian oil flows and its impact on purchases from the Middle East is dominating the discussion on trade flows, rising oil prices is throwing up new challenges for the economy. In a wide-ranging discussion with Sambit Mohanty, Asia Energy Editor, Atul Arya, Chief Energy Strategist at SP Global Commodity Insights, and Dharmakirti Joshi, Chief India Economist at CRISIL -- a unit of SP Global – share their views on the roadmap ahead for India's oil sector as the country is set to elect a new federal government.More listening options:

As a UK general election looms, energy security and the transition to net-zero are high on the agenda. In this episode of the Commodities Focus podcast, our experts sift through the policy options, from windfall taxes to licensing bans, and discuss why they matter, not just for the UK, but for Europe and beyond. Nick Coleman, senior editor for oil news, is joined by Gethin Baker, senior technical research analyst specialising in the North Sea, and Stuart Elliott, news reporter focusing on the UK and European gas markets.Explore our interactive Energy Security Sentinel™Related Price Assessments: PCAAS00 Dated Brent GTFTX00 Dutch TTF Eur/MWh Day AheadMore listening options:

Americans love pick-up trucks, and the original equipment manufacturers (OEMs) that make them rely on their relatively high profit margins to fuel earnings. Darragh Punch joins EnergyCents with hosts Hill Vaden and Sam Humphreys to discuss North America’s love affair with pick-up trucks and why electrifying them could be so important to mass EV adoption in the United States.Learn more about SP Global Commodity Insights energy coverage at: https://www.spglobal.com/commodityinsights/enJoin the conversation at energycents@spglobal.comMore listening options: