Shell flags weak Q4 refining ahead of Singapore selloff

Shell on Jan. 8 highlighted a weak fourth quarter for its refining and chemicals unit due to lower margins and a maintenance impact on throughput, as it warned investors of an expected financial impairment of $2.5 billion-$4.5 billion, primarily in the downstream.

Shell said in December it plans to offload its 500,000 b/d Singapore refining and chemicals operations due to a lack of advantage in feedstock, energy and utility costs, starkly contrasting with the company's earlier enthusiasm for opportunities in Asia in the previous decade.

Shell's global indicative refining margin dropped from $15.72/b in Q3 2023 to $10/b in Q4, and it said it expected significantly lower results from chemicals and products trading compared with Q3, with the chemicals and products unit set for an adjusted earnings loss.

Results were also affected by a slump in refinery throughput to a range of 78%-82%, a level reminiscent of the pandemic, but due to planned maintenance at its North American refining operations.

Shell's North American downstream business is spread across two sites in Canada and one in the US: the 100,000 b/d Scotford refinery in Alberta, which processes synthetic crude derived from oil sands, and the 85,000 b/d Sarnia refinery near Ontario, as well as the 250,000 b/d Norco refinery in Louisiana. Scotford was expected to operate at reduced levels during maintenance in October, while Norco was expected to be under maintenance for most of that month, S&P Global Commodity Insights reported earlier.

Elsewhere in its business, there were some signs of more stable upstream production, with the midpoint of Shell's guidance for the upstream unit higher than output in Q4 2022. It forecast production in a range of 1.83 million-1.93 million b/d of oil equivalent, offset by a potential fall in production in the LNG-focused Integrated Gas unit, to 880,000-920,000 boe/d.

Shell's oil output declined significantly between 2019 and 2022, and particularly during 2022.

Shell confirmed its earlier guidance that LNG liquefaction volumes for Q4 2023 were higher than a year earlier, in a range of 6.9 million-7.3 million mt, although that is also significantly below pre-2022 levels.

It added that financial results from LNG trading were expected to be "significantly higher" than in Q3 2023 due to "seasonality and increased optimization opportunities."

The Platts Dated Brent benchmark was assessed $4.53/b lower on average in Q4 2023 compared with a year earlier at $84.34/b. Platts is part of S&P Global Commodity Insights.

News

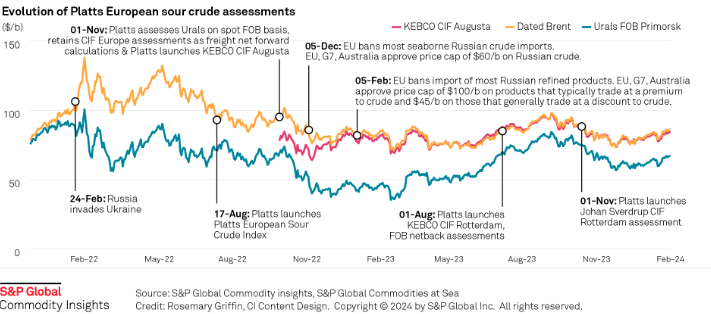

Russia's invasion of Ukraine has had a profound impact on sour crude export destinations, and increased the appetite for sweet crudes among European refiners. Platts methodology has evolved to reflect this changing landscape. Click here to see the full-size infographic.

News

Coal production to hit all-time low of 489 mil st Coal to cede generation share to renewables Nominal average delivered coal prices at $2.49/MMbtu The US Energy Information Administration Jan. 9 revised downward its 2024 coal export projection to 91 million st, which if realized would be 9% lower than 2023 exports of 100 million st. The EIA's January Short-Term Energy Outlook marked a 2.7% downward revision on the month for 2024 projected coal exports. Coal exports in 2025 are projected to recover 4.8% on the year to 95.4 million st. Lower coal demand was reflected in the EIA's 2024 US coal production estimate representing an all-time low. The EIA projected that coal production will fall 15.9% on the year to 489.3 million st in 2024 before declining another 12.4% year on year to 428.8 million st in 2025. Total coal consumption was projected at 391.3 million st in 2024, up 1.6% from the prior month's projection. The EIA estimated 2025 total coal consumption at 361.7 million st. For the electric power sector, coal consumption was estimated at 351.9 million st in 2024, down 8.4% from the prior year. For 2025, electric power sector coal consumption was projected at 322.2 million st, which would be an all-time low if realized, according to EIA data going back to 1997. Nominal average delivered coal prices were estimated at $2.49/MMbtu in 2024, down from $2.52/MMBtu in 2023. The EIA projected that 2025 nominal average delivered coal prices would shrink further to $2.44/MMBtu. Platts assessed US over-the-counter Central Appalachia 12,500 Btu/lb CSX rail coal for February delivery unchanged on the session at $72.40/st Jan. 8, showed data from S&P Global Commodity Insights. The assessment was based on broker indications of value at $72/st and $72.75/st, tested in the market through 4:30 pm ET. The Jan. 8 CAPP assessment at $72.40/st was equivalent to $2.896/MMBtu. The CAPP coal price averaged $81.12/st in 2023, the equivalent of $3.245/MMBtu. Powder River Basin 8,800 Btu/lb rail coal for prompt-month delivery closed at $13.95/st Jan. 8, unchanged on the session, based on broker indications of value at $13.85/st and $14/st. The assessment at $13.95/st was equivalent to $0.793/MMbtu. The coal averaged $14.46/MMbtu in 2023, the equivalent of $0.822/MMBtu. In line with falling coal consumption, coal's share of US power generation is expected to slip to 14.8% in 2024, down from 16.6% in 2023. The EIA projected coal generation at 13.3% in 2025 as renewables generation increases. Renewable energy sources totaled 21.8% of 2023 US generation share. Generation from renewables was projected to rise to 24% in 2024 and 25.9% in 2025. Nuclear generation's share was estimated to remain steady between 19.2% and 19.3% between 2024 and 2025. Natural gas generation, which constituted 41.9% of the US generation share in 2023, was projected to fall to 41.5% in 2024 and 41.1% in 2025. The EIA estimated that the Henry Hub spot price will average $2.76/MMbtu in 2024, down from the December 2024 estimate of $2.90/MMBtu. For 2024, the EIA projected Henry Hub prices at $3.06/MMBtu. The prompt-month NYMEX Henry Hub natural gas futures contract settled at $2.98/MMBtu Jan. 8, according to CME Group data. In 2023, the Henry Hub price averaged $2.665/MMBtu. Dry natural gas production was estimated at 105.04 Bcf/day in 2024, up from 103.54 Bcf/d in 2023. The EIA estimated that dry natural gas production would increase to 106.38 Bcf/d in 2025. LNG exports are expected to rise 4.4% on the year to 12.36 Bcf/d in 2024 before jumping 16.7% year on year to 14.42 Bcf/d in 2025. Total natural gas consumption for 2024 was projected at 89.91 Bcf/d, up 1.1% on the year. Total consumption of natural gas was projected to fall 0.2% on the year to 89.71 Bcf/d in 2025. Natural gas consumption in the US power sector was projected to rise 1.1% on the year to 35.54 Bcf/d in 2024. The EIA estimated that 2025 natural gas consumption in the US power sector will decline 0.7% on the year to 35.29 Bcf/d.

News

Sumas spot gas down 90.6% year on year CAISO solar generation up 6 points in Dec US West power forwards are trending roughly 50% lower than year-ago packages on weaker gas forwards and above-normal temperatures forecast with El Nino weather conditions to linger into spring. El Nino conditions, which typically occur January through March, tend to bring more rain to the US Southwest and warmer-than-normal temperatures. The three-month outlook indicates a greater probability for above-normal temperatures across most of the Western US, with the exception of the Desert Southwest, according to the US National Weather Service's Climate Prediction Center. SP15 on-peak January rolled off the curve at $55.75/MWh, 79.4% lower than where the 2023 package ended, according to data from Platts, part of S&P Global Commodity Insights. The February package is currently in the low 50s/MWh, 70% below where its 2023 counterpart was a year earlier, while the March package is in the mid-$30s/MWh, 55.4% lower. In gas forwards, SoCal January rolled off the curve at $3.779/MMBtu, 97.9% below where the 2023 contract ended a year earlier, according to S&P Global data. The February contract is currently around $4.063/MMBtu, 78.9% lower than its 2023 counterpart at the same time last year, while the March contract is about $2.816/MMBtu, 63.2% lower. Gas plants burned an average of 1.815 Bcf/d in December to generate an average of 267.167 GWh/d, an analysis of S&P Global data showed. That's down 0.66% from November and a drop of 11.2 % from 2023. S&P Global forecast CAISO's gas fleet to generate around 220 GWh/d in February. In comparison, burning fuel at the same rate as February 2023 would consume 1.758 Bcf/d, a 6% decrease year on year. Spot markets In spot markets, power prices were down significantly from a year ago, when cold weather hit the region and drove up prices. SP15 on-peak day-ahead locational marginal prices averaged $43.49/MWh in December, 83% lower year over year and 11.2% below November prices, according to California Independent System Operator data. Helping pull down power prices, spot gas at SoCal city-gate was down 88.4% year on year and 40% lower month on month at an average of $3.554/MMBtu in December, according to S&P Global data. In the Northwest, Sumas spot gas was down 90.6% year on year at an average of $2.669/MMBtu. The decline in spot gas prices likely accounts for the lower average spot power prices month on month in December, said Morris Greenberg, senior manager with the low-carbon electricity team at S&P Global. Compared to a year earlier, CAISO population-weighted temperatures averaged 8% higher in December, resulting in 38.4% fewer heating-degree days, according to CustomWeather data. Fuel mix Thermal generation remained the lead fuel source at 46.1% of the total fuel mix in December, little changed year on year, while solar generation was up nearly 6 percentage points to average 14.7% of the mix, according to CAISO data. Hydropower remained strong, averaging 8% of the December fuel mix, 2 points higher than a year earlier. Total generation was down nearly 8% from a year earlier at an average of roughly 23.4 GWh/day, as peakload slipped 2% year on year to average 27.254 GW in December, according to CAISO data. In the Northwest, peakload dropped nearly 11% year on year to average 7.89 GW in December, according to Bonneville Power Administration data. Hydropower remained the lead fuel source at nearly 74% of the mix, followed by nuclear at 12.3%, thermal at 9.6% and wind at 4.3%. Following El Nino expectations of the Northwest for warmer temperatures and drier precipitation, BPA population-weighted temperatures in December were 10% above normal and 21.5% higher than a year earlier, leading to 27% fewer heating-degrees days year on year, according to CustomWeather data.

News

EU projects total over 20 million mt/year of DRI by 2030 DR pellet supply gap with demand projections in 2033 Steel decarbonization may need to depend more on scrap, material innovations The scale of new European steel projects focused on bringing on more than 20 million mt of direct-reduced iron capacity using natural gas and hydrogen by 2030 may pressure available iron ore pellet supplies, spurring further innovations while potentially delaying a wider rollout of lower-emission steel. New DRI and electric arc furnaces that ArcelorMittal, Salzgitter, Voestalpine, and others planned in Germany, Sweden, Spain, and other European countries will depend on scarce low impurity direct reduction-grade pellets, with 20 million mt/year of DRI demand requiring around 30 million mt in pellets. Further growth in DRI plants may be expected next decade, despite many projects yet to achieve final investment decision and funding. While pellet availability to meet new DRI projects may be tight, markets suggest that current pellet supply can comfortably meet demand into 2024. Pellet premiums in spot markets were weak in 2023, with low premiums for higher silica and alumina blast furnace pellets imported to China from India and other origins. Contract-grade premiums for higher quality BF and DR pellets were unable to return closer to highs seen last year and in 2021, even with talk of increases for DR pellet premiums agreed for the first quarter. Low premiums also reduced the incentive to invest in beneficiating iron ores to higher pellet specifications. A mix of weaker European and global steel demand since mid-2022, low steel prices, and margins limited pellet demand. The smaller DR segment benefitted as the overall pellet market loosened. Conversely, global spot reference hard coking coal prices have remained stubbornly high, with Platts Premium Low Vol at above $300/mt FOB Australia through the fourth quarter on limited global supply expansion and spot demand led by India. Prices have trended around double operating costs, boosting miner's margins. Iron ore supply Iron ore supply may see limited growth potential outside a handful of existing high-grade projects for global iron ore resources to economically bring on DR-quality feed. This may need innovation in adapting steelmaking processes to remove coal and use lower quality iron ores, as well as putting the onus on ferrous scrap supply—in both volumes and low residual metal grades to meet steel quality and drive steel decarbonization. US Steel is planning to supply DR-grade pellets from its Keetac taconite ore operation in Minnesota, with specific qualities and shipment schedules yet to be discussed in the market since an earlier end 2023 production target. ArcelorMittal Mining Canada is pivoting to produce DR pellets from its current mix with blast furnace grades following new investments. Even with the change, the Canadian operation would fall well short in meeting ArcelorMittal's DRI project needs. Other existing pellet suppliers may tweak output and production volumes with investments and licenses, while DRI operators in Algeria plan to expand iron ore processing and pelletizing, investing in dedicated plants and buying in concentrate iron ore from global sources, currently including Mauritania. Forward DR pellet supply tightness may be exacerbated by the ongoing war in Ukraine affecting iron ore supplies from Ukraine and Russia, new investments in the region, and developing new markets and trade flows ahead of new DRI plants coming online in Europe from around late 2025. Based on typical blast furnace iron ore burdens in western Europe, pellet demand for DRI may be around three to four times higher, even in cases where lump ore is utilized together with pellets. For steel producers such as SSAB, Cleveland Cliffs, US Steel, Stelco and other North American blast furnace operators running on 100% pellets, or pellets with hot-briquetted iron and scrap, the difference in demand for pellets with DRI plants may be limited, putting pressure on Europe to find additional volumes. The difference would also depend on DRI quality and usage in EAFs with ferrous scrap and yield efficiencies. DR quality The direct reduction route is more sensitive to iron ore quality and market-based iron ore pellet supply will be crucial, according to the International Iron Metallics Association. The IIMA forecasts a gap in 2033 of around 34 million mt in DR-grade iron ore pellets factoring in demand growth from global DRI plants, in a November presentation. Even with some lower-quality blast furnace pellets being used for DRI, the IIMA estimates a remaining gap of 18 million mt—equivalent to around 12 million mt/year of DRI capacity or 5 DRI modules short of feed. DRI plants cannot use slag to remove impurities and control iron quality, as well as production rates. DRI plants need pellets with low alumina and silica to optimize DRI quality, to limit effects on energy consumption and quality in downstream steelmaking processes. Outside Europe, existing DRI producers reliant on imported pellets may expand demand, consider new iron ore briquettes, and spur on new iron and steel projects with projects to harness renewable power and carbon capture, utilization, and storage. Major DRI producers in Saudi Arabia, Egypt, the UAE, Algeria, Trinidad & Tobago, and Malaysia, along with new DRI projects in China and Russia, may push iron ore producers to expand further. Investment using lower-quality iron ore and the direct reduction of iron ore fines, among other technologies may gather pace after passing tests. South Korea, China, and Japan are eying DRI and EAF investments, with projects to establish lower emissions metallics supply and better utilize scrap and existing blast furnace raw materials and processes in combination with miners BHP, Rio Tinto, and others. "Increased scrap recycling and mass deployment of innovative technologies are key levers for reducing emissions," the International Energy Agency said in a September report.